MP Board Class 12th Accountancy Important Questions Chapter 4 Reconstitution of Partnership Firm: Retirement / Death of a Partner

Reconstitution of Partnership Firm: Retirement / Death of a Partner Important Questions

Reconstitution of Partnership Firm: Retirement / Death of a Partner Objective Type Questions

Question 1.

Choose the correct answer:

Question 1.

Abhishek, Rajat and Vivek share profit and loss in the ratio 5 : 3 : 2. If Vivek retires from the firm, new profit sharing ratio between Abhishek and Rajat will be:

(a) 3 : 2

(b) 5 : 3

(c) 5 : 2

(d) None of these.

Answer:

(b) 5 : 3

Question 2.

Rajendra, Satish and Tejpal share profit and loss in the ratio 2:2:1. After Satish’s retirement, new profit sharing ratio between Rajendra and Tejpal is 3:2, then their gaining ratio will be:

(a) 3 :.2

(b) 2 : 1

(c) 1 : 1

(d) 2:2.

Answer:

(c) 1 : 1

Question 3.

Anand, Bahadur and Chander share profits equally. After Chander’s retirement Anand and Bahadur acquire chander’s share in the ratio 3 : 2. New ratio of Anand and Bahadur will be:

(a) 8 : 7

(b) 4: 5

(c) 3 : 2

(d) 2 : 3.

Answer:

(b) 4: 5

Question 4.

In the absence of any provision, the remaining partners acquire the share of retiring / deceased partner in:

(a) Old profit Sharing ratio

(b) New profit sharing ratio

(c) Equally

(d) None of these..

Answer:

(a) Old profit Sharing ratio

![]()

Question 5.

On retirement / death of any partner, his capital A/c will be credited with :

(a) His share of Goodwill

(b) Firm’s Share of Goodwill

(c) Remaining partner’s share of Goodwill

(d) None of these.

Answer:

(a) His share of Goodwill

Question 6.

Govind, Hari and Pratap are partners. On retirement of Govind, Goodwill account appears in the books of the firm worth Rs. 24,000. Goodwill will be writen off by:

(a) Crediting all partner’s capital account in old ratio

(b) Crediting remaining partner’s capital account in new ratio

(c) Crediting retiring partner’s capital account with his share

(d) None of these.

Answer:

(a) Crediting all partner’s capital account in old ratio

Question 7.

On retirement of a Partner, share of other partner:

(a) Increase

(b) Decrease

(c) Increase or decrease both

(d) None of these.

Answer:

(a) Increase

Question 8.

Share of retiring partner includes :

(a) Goodwill and Share in profit

(b) Capital, Goodwill and Salary

(c) Capital, Goodwill and Share of profit

(d) Capital, Goodwill, Salary, Share in profit and Revaluation profit.

Answer:

(d) Capital, Goodwill, Salary, Share in profit and Revaluation profit.

![]()

Question 9.

Which account is opened to give share of Assets and Liabilities of the firm to the retiring partner:

(a) Revaluation A/c

(b) Realization A/c

(c) Profit and Loss A/c

(d) Profit and Loss Adjustment A/c.

Answer:

(a) Revaluation A/c

Question 10.

If a partner leaves the firm, then profit is divided among remaining partners in the ratio of:

(a) Equally

(b) Gain

(c) No change.

(d) None of these.

Answer:

(b) Gain

Question 11.

When old ratio is deducted from new ratio it is called :

(a) Sacrificing ratio

(b) Equal ratio

(c) Gaining ratio

(d) None of these.

Answer:

(c) Gaining ratio

Question 12.

After the retirement of partner the profit and loss of revaluation is distributed to:

(a) Remaining partners

(b) Retired partner

(c) All partners

(d) None of these.

Answer:

(a) Remaining partners

![]()

Question 13.

If the amount is not paid to the representative of deceased partner then what % per annum is to be given as interest: (MP 2017)

(a) 10%

(b) 5%

(c) 6%

(d) None of these.

Answer:

(c) 6%

Question 2.

Fill in the blanks:

- By gaining ratio there is an ……………. in the ratio of remaining partners. (MP 2010)

- When retired partner is paid the amount payable in annual installments, then the ac-count maintained is ……………

- In ………….. a partner can leave the firm by giving a written intimation.

- On the death of partner claim amount is given to ………………

- Life insurance reserve fund is transferred to ……………. capital account. (MP 2011)

Answer:

- Increase

- Annuity account

- Partnership at will

- Representative

- Partner’s.

![]()

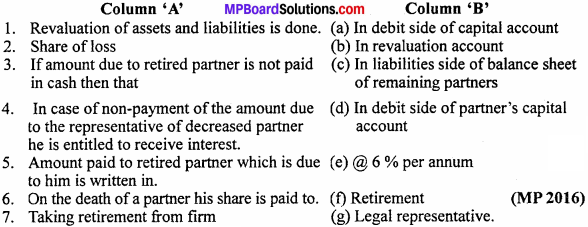

Question 3.

Match the columns:

Answer:

- (b) In revaluation account

- (a) In debit side of capital account

- (c) In liabilities side of balance sheet of remaining partners

- (e) @ 6 % per annum

- (d) In debit side of partner’s capital account

- (g) Legal representative.

- (f) Retirement

Question 4.

Write true or false:

- Retired partner can also be paid by annuity.

- Retiring partner has no right over the amount of goodwill.

- Gaining ratio is calculated when a partner is retired or dead.

- When goodwill account is opened with its full halve then goodwill account is credited.

- Increase in the value of assets is shown in credit side of revaluation account.

- A, B and C are partners in the ratio of respectively. B retires from the firm.

- Joint life policy has no surrender value.

Answer:

- True

- False

- True

- False

- True

- True

- False.

![]()

Question 5.

Write the answer in one word / sentence:

- Write one reason for the retirement of a partner. (MP 2010)

- Give me base for the calculation of profit on the death of a partner.

- In case of retirement of partner, general reserve of balance sheet should be distributed among partners in which ratio ?

- New ratio – old ratio = ?

- When does a partner retire from a firm ? (MP 2011)

- To whom the amount is paid on the death of a partner ? (MP 2012)

- Which account is opened when payment is given to a partner by annuity method ? (MP 2012)

- In whom the amount payable to deceased partner is paid. (MP 2017)

Answer:

- Old age

- Time

- Old ratio

- Gaining ratio

- Old age/expiry of term mutual agreement between partners

- Legal representative

- Annuity suspense Account

- Executor.

![]()

Reconstitution of Partnership Firm: Retirement / Death of a Partner Very Short Answer Type Questions

Question 1.

What do you mean by retirement of a partner ?

Answer:

Due to some circumstances, any partner of the firm doesn’t want to continue as a partner in the firm it is called retirement of a partner, under retirement the partner discontinued his relations from the firm.

Question 2.

Give two reasons for the retirement of a partner.

Answer:

In the following two circumstances a partner can retire:

1. Due to old age:

When a partner attains old age and he finds himself unable to do work of the partnership business, he may retire from the firm.

2. Due to ill health:

When a partner becomes the victim of such a disease that he cannot take active part in the conduct of business, he gets retirement from the firm.

Question 3.

What is gaining ratio ?

Answer:

After the retirement of a partner, the future profit-sharing ratios of the remaining partners increases automatically, since, they acquire the left out share of profit in some agreed ratio or in their old ratios. Thus, the ratio in which the remaining partners gain over their old profit-sharing is called gaining ratio.

![]()

Question 4.

What journal entries are passed when goodwill is opened and written-off?

Solution:

Question 5.

What do you mean by Legal representative ?

Answer:

Legal representative is the person for which the partner will be held responsible for the action done by him/ her. In the case of death of the partner, his executor / successor will become his legal representative and has all the rights to get the amount due to the deceased partner.

![]()

Reconstitution of Partnership Firm: Retirement / Death of a Partner Short Answer Type Questions

Question 1.

Write five circumstances that any partner can retire from the firm.

Or

In what conditions a partner can retire from the firm ?

Answer:

In the following circumstances, a partner can retire from the firm :

- Due to old age

- Due to inability

- If any partner shows personal interest

- If any partner does his duty against the contents of deed

- If the firm makes continuous loss.

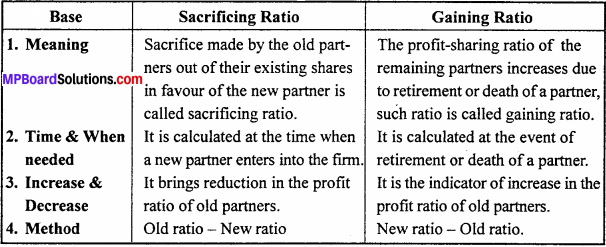

Question 2.

Differentiate between sacrificing and gaining ratio.

Answer:

Differences between sacrificing and gaining ratio:

Question 3.

Explain the rights of a retiring partner regarding the various amounts pay¬able to him.

Answer:

A retiring partner has the right to claim the following amounts till the date of his retirement:

- The balance of am-bunt shown by the capital account on current account in the last balance sheet

- Share of profit

- Share of profit on revaluation of assets and liabilities

- hare of L.I.C. Premium

- Interest on capital if any

- Share of goodwill

- Share of reserve, if any

- After entering all the above items, the balance amount is treated as the amount payable to the representative of the dead partner.

![]()

Question 4.

What are the methods prevailing to pay off the outgoing partner from the firm ?

Answer:

Following methods are generally adopted to pay off the outgoing partner:

- Payment in lump sum: When the firm has sufficient cash then the retiring partner is paid in lump sum.

- Payment through bills payable: A bills payable is issued to the partner for a specific term and when the time expires then payment is done to him.

- Payment in installment: The amount payable to the outgoing partner is treated as loan and kept in the firm. This loan is paid off in installments together with a specific rate of interest.

- Payment through annuity: The amount due to the retiring partner can be paid through annuity for certain years.

Reconstitution of Partnership Firm: Retirement / Death of a Partner Long Answer Type Questions

Question 1.

How the amount is calculated for a partner, who is retiring from the firm?

Or

How is the amount due to retiring partner determined ?

Answer:

The share of retiring partner or the amount payable to a retiring partner is calcu-lated according to the method mentioned in the partnership deed:

(1) Amount receivable by a retiring partner from the firm:

- Balance of his capital as per the last closing balance sheet.

- Interest on capital and share of profit up to the date of retirement, provided in partnership deed.

- Salary, bonus, commission etc, if provided in the partnership deed.

- Profit on revaluation of assets and liabilities of the firm.

- Share of goodwill.

- Share of undistributed profits, reserves, funds etc.

- Any other amount receivable from the firm as per the partnership deed.

(2) Amounts payable by a retiring partner to the firm:

- Debit balance of his capital account as per the last balance sheet, if any.

- Drawings and interest on drawings.

- Share of loss on revaluation of assets and liabilities.

- Share of loss up to the date of retirement, if any.

- Any other amount payable by the retiring partner to the firm

(3) After crediting and debiting the above amounts in the capital account of retiring partner, the balance is drawn which represents the final amount payable to the retiring partner.

![]()

Question 2.

Explain the method for opening goodwill account on retirement of partner and write the journal entries.

Answer:

Method for opening goodwill account on retirement of partner and the journal entries are as under :

(a) When goodwill account does not exist in the books : After calculating the share of the deceased partner, the following journal entry is passed:

Remaining partner’s Capital A/c Dr.

To retiring partner’s Capital A/c

(Being adjustment of goodwill done)

(b) When Goodwill already appears in the book:

(i) For writing off the old goodwill Dr.

All partner’s capital A/c

To goodwill A/c

(Being goodwill written off in old ratio)

(ii) For recording the deceased partner’s share of goodwill

Remaining partner’s capital A/c Dr.

To retiring partner’s capital A/c

(Being adjustment of goodwill made).

Question 3.

How will you calculate the amount payable to his legal representative on the death of a partner ?

Answer:

Following steps are taken to determine the share of a deceased partner payable to his legal heir:

1. Preparing memorandum final accounts until the date of death of the partner.

2. Preparing deceased partner’s capital account.

3. Posting of following amounts to the credit of his capital account:

- Balance of capital

- Interest on capital up to the date of death, if provided in partnership deed

- Bonus, commission, salary etc. if provided in partnership deed

- Share of current year’s profit up to the date of his death

- Share of undistributed profits, reserve fund and goodwill

- Share of profit on revaluation.

4. Posting of following amounts to the debit side of his capital account:

- Amount of drawings

- Interest on drawing if any

- Loan and interest on loan, if any

- Share of loss on revaluation of assets and liabilities

- Undistributed losses of the firm.

5. Transfer of deceased partner’s current account balance to his capital account, if any.

6. Share of amount of life policy if the firm has taken a joint life policy